It represents the amount of money required to acquire a substitute asset that would provide the same utility or functionality as the original asset. Replacement cost is often used in financial valuation to assess the value of assets, especially in industries where asset replacement is common or necessary for business operations. While the cost approach is popular for its ease of application, its largest drawback is the subjectivity related to input parameters that are chosen—particularly with respect to obsolescence. With regard to the reproduction cost method, it fails to reflect the actual market demand for the asset and hence neglects the possibility that a third party might not want an identical replica on the valuation date. Furthermore, opportunity costs are often insufficiently reflected in the cost base.

Our Services

Also, the replacement costs of three assets are $80,000, $100,000, and $150,000, respectively. When depreciation is charged on historical cost, it will not match the cost of the replaced asset. Some assets are depreciated on a straight-line basis, meaning the cost of the asset is divided by the useful life to determine the annual depreciation amount. Other assets are depreciated on an accelerated basis so more depreciation is recognized in the early years and less in later years. The total depreciation expense recognized over the asset’s useful life is the same, regardless of which method is used.

The Cost Approach

When a company is evaluating the scenario of replacing an asset it is very important to consider the profitability of the purchase at the new cost. Since the newly purchased asset might be more expensive than the old asset, the new purchase must be evaluated carefully to see if the net present value of the investment stays positive considering the new price of the asset. After conducting market research, ABC Inc. determines that similar trucks with the same specifications and features are currently priced at $60,000 each in the market. Therefore, the replacement cost of each truck is $60,000, reflecting the amount ABC Inc. would need to spend to acquire a new truck with similar capabilities. The insurance company’s primary function is to evaluate whether the decision of replacement is better than repair and maintenance.

- An organization often chooses to replace its assets when the repair and maintenance costs increase beyond an acceptable level over some time.

- The paper seeks to stimulate debate on the current professional guidance for the use of the replacement cost method of valuation.

- The total depreciation expense recognized over the asset’s useful life is the same, regardless of which method is used.

- CoreLogic continually monitors changing market conditions throughout the U.S. and Canada and makes appropriate adjustments for these situations when necessary.

Business Valuation

Replacement cost can also be used to estimate the amount of funding that might be required to duplicate another business. This concept can be used to establish one of several possible price points that can be used in the formulation of a proposed price to pay the shareholders of a target company as part of an acquisition. Replacement cost is the cost involved in replacing an existing item with another item having same or similar features. Businesses can assess the depreciation cost of the item against the market value of the same and then decide whether to replace it. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

All of our content is based on objective analysis, and the opinions are our own. The cost to replace an asset can change, depending on variations in the market value of the asset and other costs needed to get the asset ready for use. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. Although the concepts of market value and reconstruction cost are different, both are affected by economic conditions.

It is also vital for a company to correctly calculate the depreciation since it will have a significant impact on the decision to continue the old asset or replace it with a new one. Sometimes it becomes a challenge to estimate the correct market value of the asset, and hence it may lead to making wrong decisions by the organization. The main limitation with replacement Cost Accounting is that it only works well under certain circumstances, such as when there has been no capital gains tax and indexation has not played a part in any real property investment decisions. It is also important to note that replacement Cost Accounting should not be used for intangible assets. Rca requires the appropriate index numbers to be used when replacing old assets, which means it does not result in any loss. By using rca instead of cpp you make provisions based on the current costs the company will incur after years of use for an asset compared to the original cost of that asset.

This does not include value lost to depreciation, or changes in the market value of that property due to fluctuations in supply and demand. The supply and demand for housing also impacts the fair market value, just as the supply and demand for labor and materials affect replacement cost. When situations arise where supply does not match or equal demand, market value and the replacement cost can change quickly.

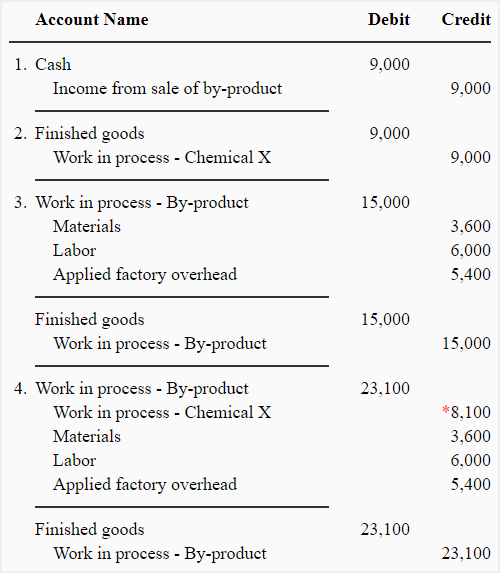

The replacement cost method is an accounting approach that values assets based on the cost to replace them with new ones at current market prices. This method is particularly useful for evaluating the worth of by-products, as it considers the expenses involved in producing or acquiring replacements rather than their historical costs. By focusing on current values, this method helps businesses make informed decisions regarding resource allocation and pricing strategies. The cost approach indicates an intangible asset’s value by considering its replacement or reproduction cost, relying on the economic premise that a prudent investor would pay no more for an asset than the cost to acquire an asset of equal utility. The cost approach is typically applied for the valuation of a workforce—a key component of a firm’s goodwill and a crucial input for the income approach to valuing intangibles. Replacement cost is the price that an entity would pay to replace an existing asset at current market prices with a similar asset.

Thus, $23,000 is the replacement cost of the $20,000 truck because this is how much it would cost to buy that same truck today. The company should make a wise decision by carefully calculating this cost by comparing its repair and maintenance costs, which can be levied over the years if the asset is not replaced. A business then considers accounting for contingent liabilities the cash outflow for the purchase and the cash inflows generated based on the increased productivity of using a new and more productive asset. The cash inflows and outflow are adjusted to present value using the discount rate, and if the net total of all present values is a positive amount, the company makes the purchase.